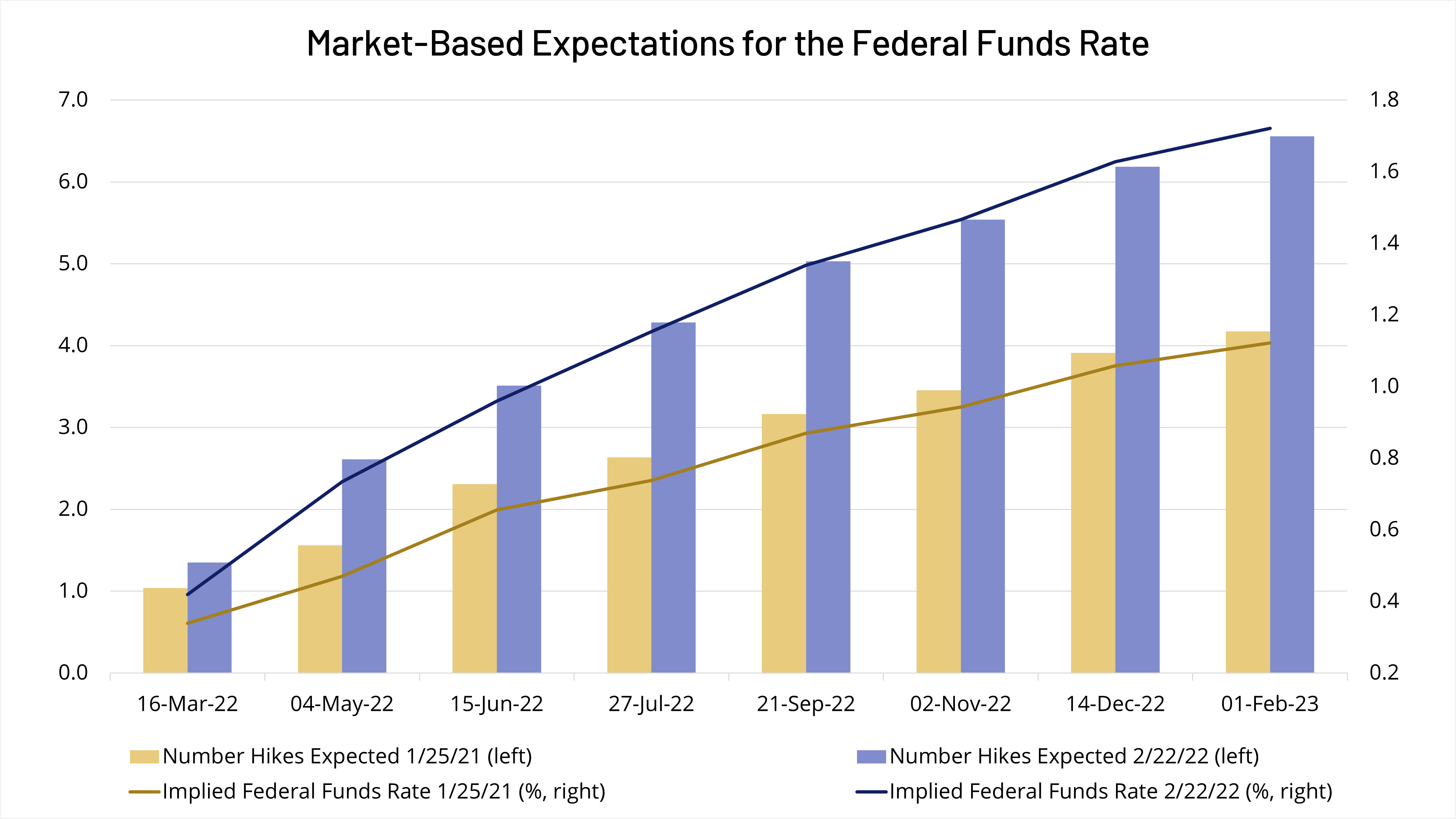

- December 3, 2024

- Posted by: Visa Imigration

- Category: cash advance and payday loans

The lender will more than your financial details and then make good choice. When the accepted, you will get a great preapproval letter – our very own relatives from the Skyrocket Mortgage can offer you a verified Acceptance Letter (VAL). This new page will state a certain amount the financial institution is actually ready to help you provide you and in the event that give will expire. You’re able to consult improvements with the preapproval page, with regards to the cost of land you are making has the benefit of on. Including, if you’re trying to find a property detailed for $175,000 plus preapproval page claims you happen to be recognized as much as $2 hundred,000, it is possible to request that your particular letter be up-to-date so you’re able to the low number, understanding you’ve got the discussing capability to increase your preapproval matter if you can find competing now offers to your possessions.

Regardless of if it’s not technically part of the financial preapproval application process, this step may be worth these are. To simply help enhance your chances of bringing a final recognition getting home financing, hold off to the to make one large requests otherwise taking out a separate loan. Your mortgage preapproval will be based upon your current financial predicament, and you can significantly switching it could apply to how much you can get into the investment, if any after all. If you do intend on while making a big buy, consult the bank as you’re submitting papers to find out if that will connect with the choice.

How much time does financial preapproval past?

How much time a home loan preapproval persists is dependent on the financial institution, though it normally covers from 30 180 days. An average of, you can expect a home loan preapproval letter to help you last up to 90 months. To see how long the preapproval letter you certainly will history, speak with the bank.

Could it possibly be beneficial to locate a great preapproval to own a home financing?

It could be worth every penny to get an effective preapproval getting good home loan since you generally have a better understanding of how much you can afford to cover a house. Including, it can also help you restrict your choices in the event it involves deciding on belongings you to slide within your budget. Whether or not it’s not good seller’s marketing, which have a home loan preapproval is beneficial because reveals a property agencies and you may house providers that you will be into the an effective place economically and therefore are dedicated to to get a home.

Just how long can it shot rating home financing preapproval?

The length of time it will require to track down home financing preapproval all hangs into the bank. Quite often, the process can take as little as a short while, just in case the financial institution obtains any suggestions in due time. Although not, whether your lender means much more files from you, then the procedure might take lengthened.

How far aside do i need to get preapproved for a mortgage?

Providing a great preapproval to own home financing may appear at any time do your real estate techniques. Remember that the loan preapproval page does end, therefore you need to have time to look available for a property ahead of one expiration time. You ought not risk risk obtaining the mortgage preapproval letter expiring, and having to endure the method once more.

Create financial preapprovals affect borrowing from the bank?

In many cases, mortgage preapprovals require a hard borrowing from the bank eliminate, that will briefly lower your credit history. Ask your financial to find out if that’s the instance before distribution the documents.

What takes place easily don’t get preapproved for a mortgage?

If you get refused for a mortgage, really lenders deliver a description precisely why you were not recognized. Whether or not not, you have the directly to contact the financial institution significant hyperlink locate good justification because of their ple, maybe the debt-to-money (DTI) proportion try too high, otherwise you will be self-functioning and cannot developed dos years’ value of funds and you can losings statements. Whatever the reason could be, simply take these into account or take enough time to switch all of them before you apply again. If the DTI try higher, measures you might capture is settling obligations otherwise looking indicates to improve your earnings. Otherwise, you may need to hold back until you have many years of tax returns when you’re a home-employed private.