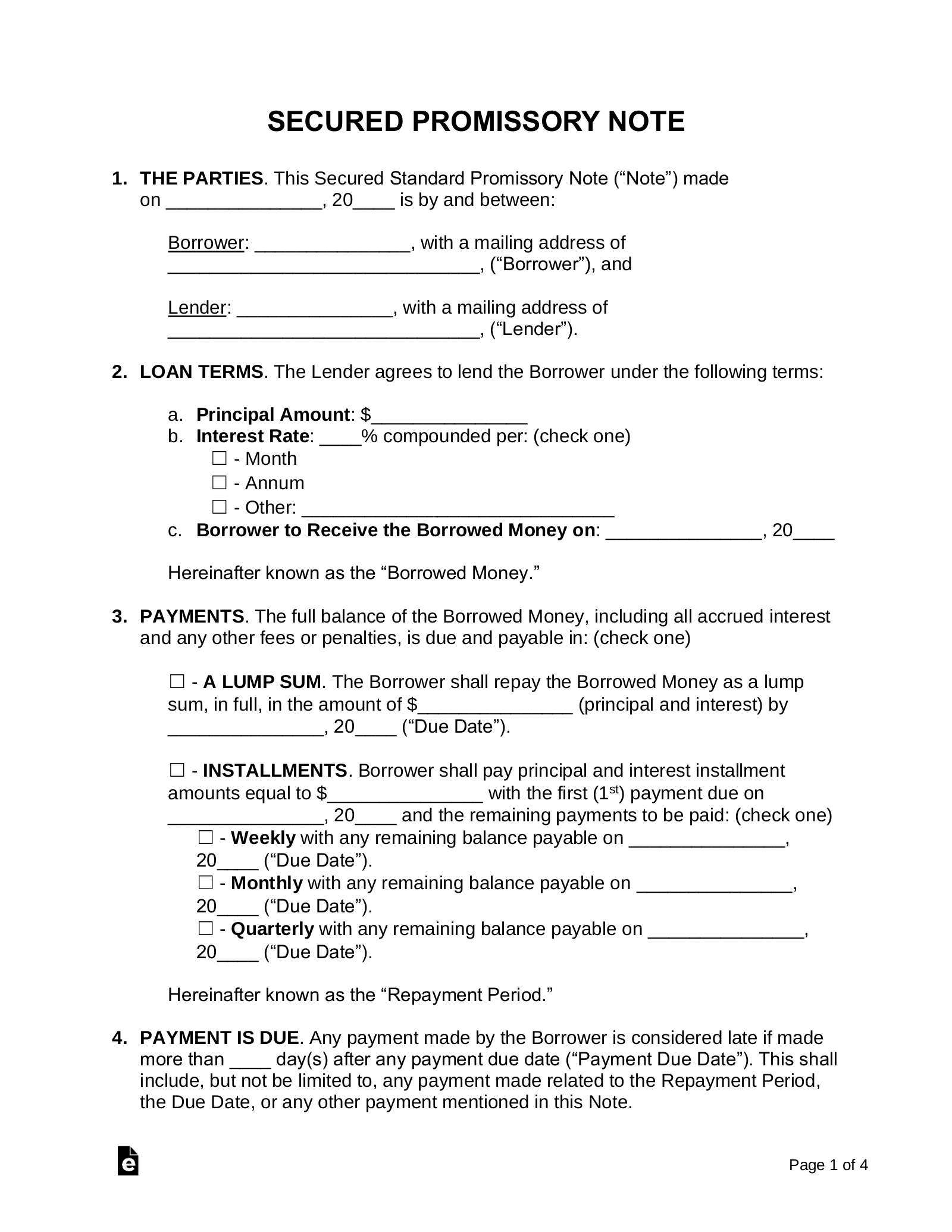

- January 22, 2025

- Posted by: Visa Imigration

- Category: loans for payday

- Japanese Citizens and you may Permanent Residence people can go to any financial and might be eligible for 0 deposit finance.

- Visa-holders have a much narrower variety of bank options, and you may typically have to lay 20% downpayment however, rates may be the exact same.

- Often circumstances, make an effort to reveal Japanese earnings* for the past year (ideally many years). From this What i’m saying is try to keeps filed taxation $255 payday loans online same day North Carolina inside the The japanese.

- Your income stubs into the The japanese along with your taxation filings are just what very matters (for those who have never assume all months otherwise half-year to your tax filings, you may need to wait a different sort of season to maximum out your borrowing prospective).

- The overseas income will not really amount (a residential property leasing income, and low-japan taxable income).

- The level of dollars or assets you really have will most likely not matter.

We authored will most likely not count during the last 2 factors due to the fact on the surface it generally does not make it easier to qualify, nonetheless it can help you a tiny at later on phases We tune in to.

In the The japanese, our home loan (jyuutaku ??) is actually for your primary home merely and you must live there. If you disperse at some point in The japanese otherwise to another country, the bank needs you to definitely offer our house because you no lengthened real time truth be told there, otherwise re-finance as a good investment otherwise next home.

There’s an impact anywhere between a first resident mortgage and you can a second house against an investment loan

These types of pried first maximum loan computation was 7x your own annual income (I believe it is their overall taxable revenues along with bonuses an such like – ie, the amount in your tax filing, as opposed to your own month-to-month gross paycheck * 12). Certain say 10x – however it you will trust which count you employ since the multiplier.

- Overseas a home – oddly/unfairly they make the financing commission under consideration, yet not the latest local rental money (??)

- Money a residential property financing – a few banking institutions dont is whole strengthening capital real estate (Aruhi to own such), but most commonly amount them facing the max borrowing limit

- Almost every other bills like handmade cards otherwise loan-shark debts (just kidding towards second, men and women wouldn’t amount however you possess bigger problems in daily life..)

Japan are a nation who’s got highest value for the character, steady work records, life tale, etcetera. And therefore warning flags getting finance companies:

The first and you will 2nd affairs try searched because of the files your fill out. The 3rd area music uncommon to help you westerners because enjoys nothing financial influence – however, Japanese Finance companies want to see/listen to their plan very establish they undoubtedly. Negative and positive factors:

My personal insights would be the fact most financing was myself stored because of the finance companies and are Perhaps not Flat35. Such banking institutions often keep loans, resell, or bundle since individual question MBS products. A few secret aspects of Flat35 vs Private which is either counter-easy to use

You will find obtained 4 mortgage / possessions money inside the Japan so far – I am not saying a professional, but I might say I have specific experience

I did not see which prior to, nevertheless seems the brand new Flat35 system is for highest-exposure applicants, and this higher cost and you may charges. Specific banks offer each other personal and Flat35’s having superior consumers bypassing the newest Flat35 solution.

initially 2 factors is actually interesting – home loan prices echo the brand new funding costs, and resource rates in The japanese try close 0 (if not negative). Both unsecured debt and you may corp debt is associated with it low priced financial support to perform the country. A growth of just one or dos full percentage circumstances create break the latest economy due to the fact organizations consistently must replenish financial obligation investment, and you may do unexpectedly getting against an emergency. Hence you will be able/possible that prices have a tendency to creep up, but it’s hard to consider more than a beneficial 0.1% or 0.2% rise in annually.

The next part is the most important. When you’re debating a good 0.7% varying compared to a 1.2% repaired, then your 0.5% is probably incorporating six7% to your mortgage payment. If the money is rigorous, it issues, but it also form you probably cannot chance they.